Day 114

In the last couple of weeks, I crawled back some of the gains I gave up as mentioned in my previous post.

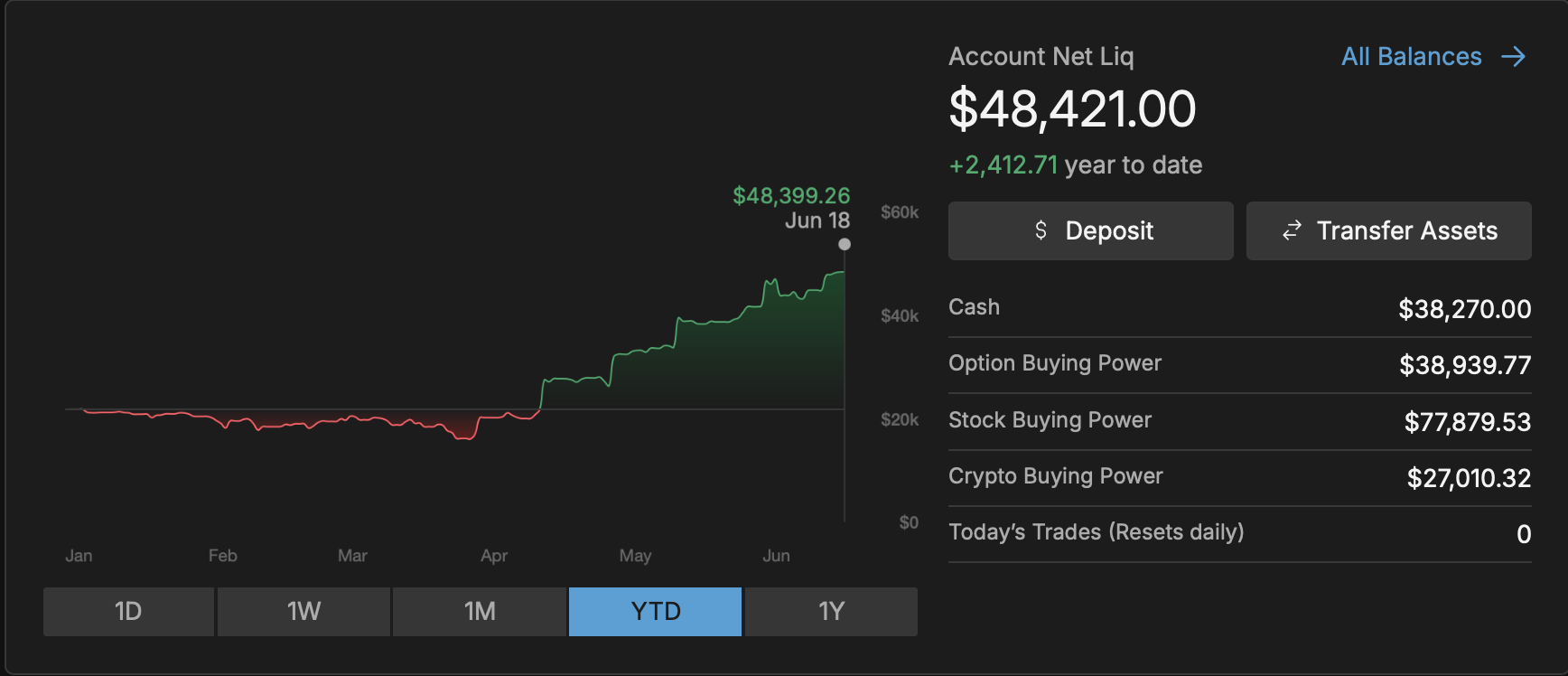

Portfolio Status

Here is the current portfolio status, including unrealized Profit/Loss. My current account balance is just over $48K, with realized gains about to touch $4K (~+8.7% return year to date).

Here is the entire Year to Date P/L list for closed positions - I added previous week's list here for comparison.

I gained $199 in realized premiums, inching up my realized gains for the year to date from $3,765 to $3,964.

Market Recap

SPY is at ~$746, and QQQ is on ~$739.

VIX is hovering around 16.

Trading Update

I had fun this time around. I traded the usual suspects such as SPX, and AAPL. And added SPCX the day they opened options trading for it.

AAPL

I was in and out of trades over a few days - selling puts slightly below expected move and selling calls at the expected move. Scalped $209 in premium via multiple such strangles.

NVDA

Sold an expected move strangle ($175/$225). Bought the call back when price moved away from call strike towards the Put, and bought the put back when price moved up. Net $125.

GOOGL

I traded Google for the first time in this account. My thesis was that a SpaceX pop may cause a ripple effect in Google, because Google had ~5% stake in SpaceX since 2015 (https://www.reuters.com/article/business/spacex-raises-1-bln-in-funding-from-google-fidelity-idUSL4N0UZ6LG/).

And since Option trading was not yet open in SpaceX at IPO launch, I used Google as a proxy. Anyway, I made a measly $29 for a Put I sold and bought back soon enough after a small move up in Google.

SOFI, UBER, SLV, HOOD

I extracted a tiny bit of premium across a few standalone/directional shorts (bearish SOFI, bullish everything else), net $143.

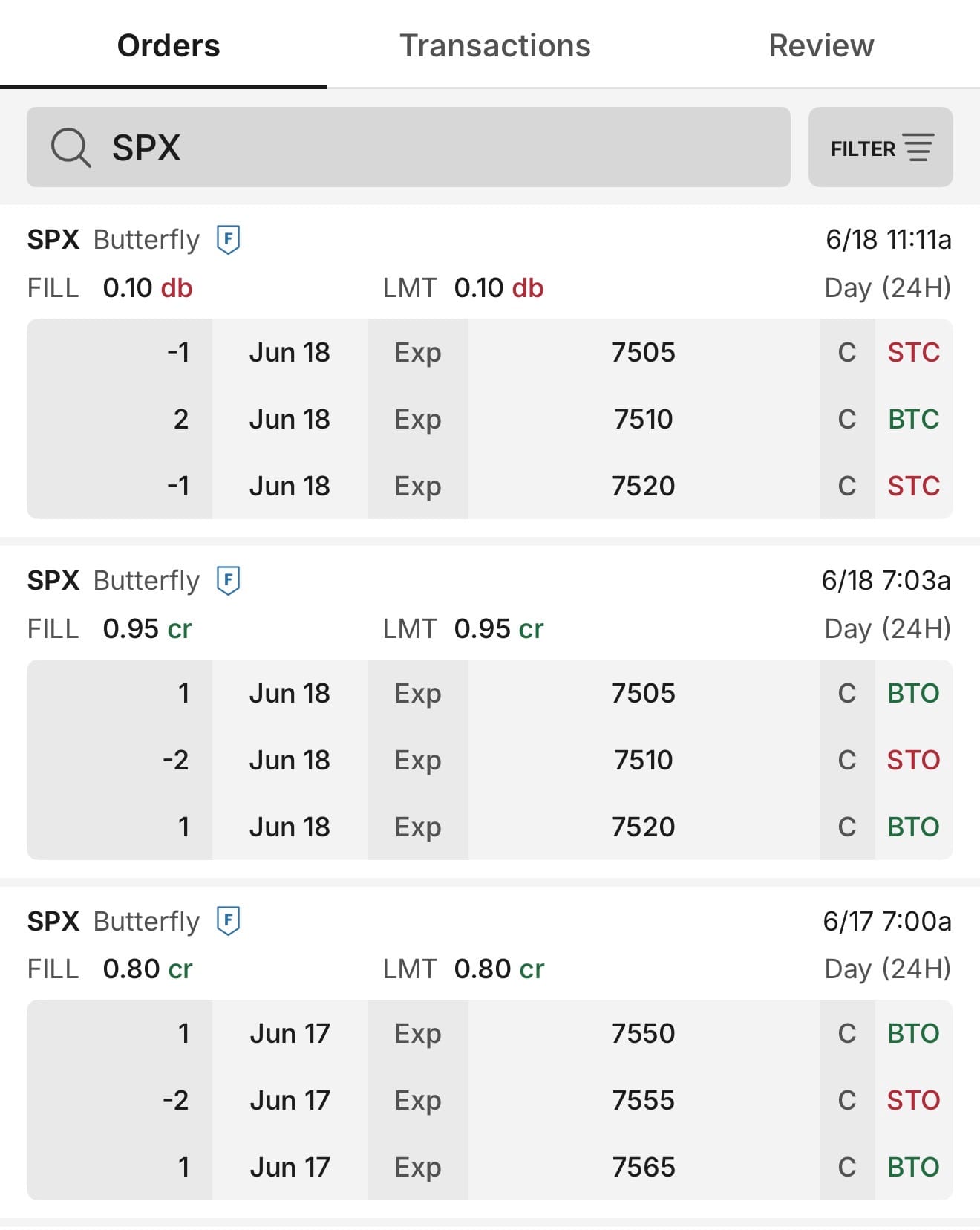

Continued Zero DTE Experiments in SPX

Like I have mentioned previously on my posts here, I love trading Zero DTE SPX. It has high liquidity and fast feedback, and so you don't have to wonder if you can get into a trade or not, or wonder for long if you are right or wrong - you know it pretty soon!

But they are also the most risky bets to place and can ruin your account fairly quick quite unlike any other trade.

I have also written about the risks of Zero DTE with a full time job. But it's a problem worth solving for me. In that spirit, I went away from Zero DTE Spreads and Iron Condors and tried a different tactic.

I was bearish in SPX and so went short and traded a broken wing butterfly (BWB).

From TastyTrade:

A broken wing butterfly is a long butterfly spread with long strikes that aren’t equidistant from the short strike.

While it may sound fancy - in execution it is fairly simple combination of two spreads - a debit spread and a credit spread - and the objective is to get more credit than debit so that the overall position results in a net credit.

I bought a $5-wide Call Spread and sold a $10-wide Call Spread on two days.

I let it expire the first time, keeping the $80 in premium as all the options expired out of the money.

The second time, I closed it when it captured >90% of premium, netting $85 in premium.

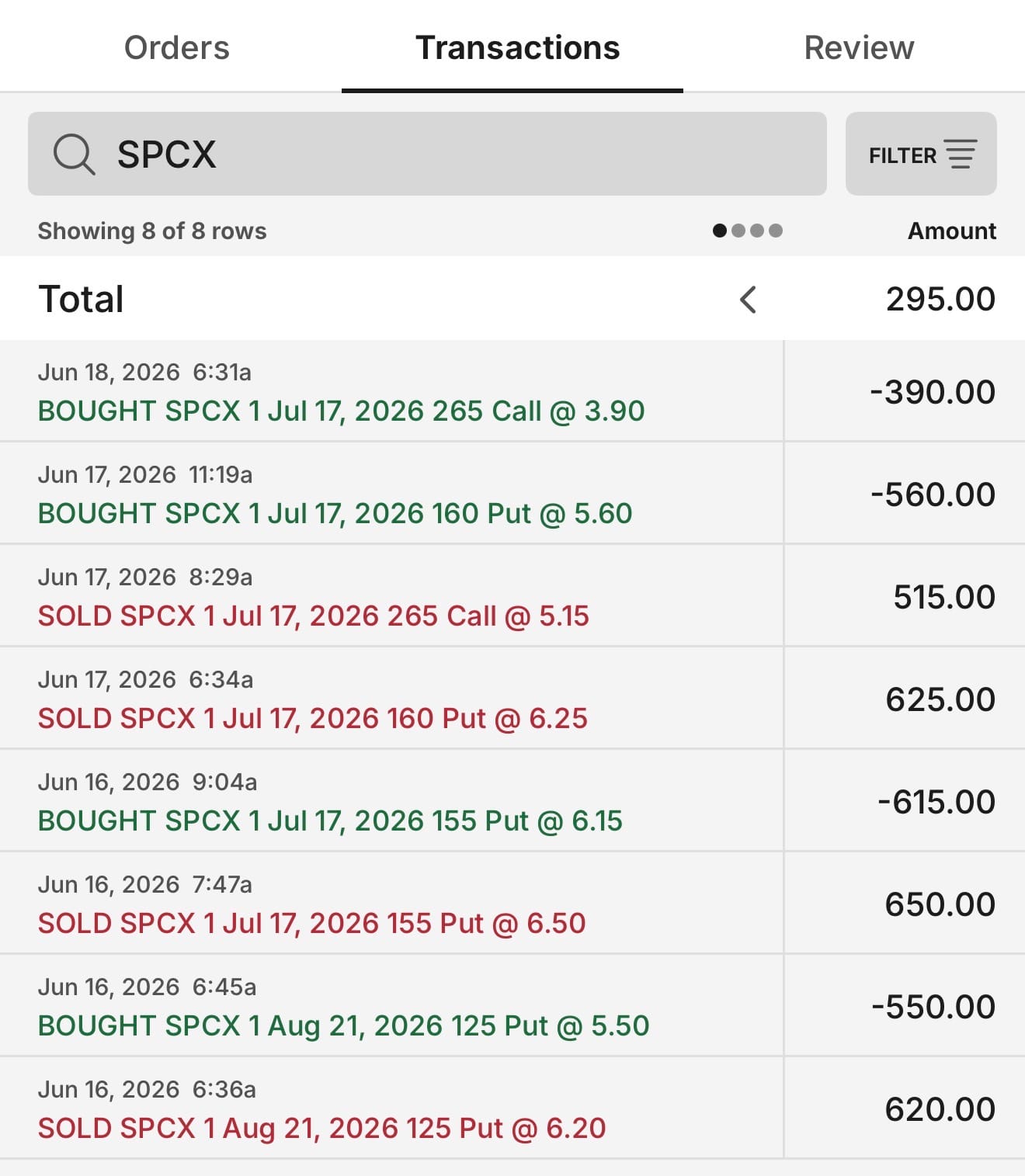

SPCX

And last but the most interesting trades I did were in SpaceX. This was a total wild ride.

The stocks were already trading from a week before, but it opened up for options on 16th.

My thesis was that some initial excitement would shoot the price up, then people would start to take profits and price might move down but still stay elevated, and then price would fall a bit more as more people begin to take profits once they start seeing the price is no longer moving up.

The thesis was completely unrelated to emotions or soundness of the company itself - but more so how a herd typically behaves in any situation around novelty in life. Do you remember Clubhouse from 2021? Invite-only access manufactured artificial scarcity, which amplified the novelty premium. Everyone wanted in. Then they got in, realized it was just people talking, and left. The app didn't get worse, we can say there was nothing wrong with the product and nothing right about it either. It was pure novelty cycling through a crowd. The herd just exhausted its curiosity and moved on.

Back to trading - I got extremely lucky and was able to make several frequent entry and exit at various price points. I did get helped by the extremely high implied volatility in SPCX.

Even right now as I am writing this, SPCX August 21, 2026 implied volatility for the $300 Strike Price is ~100%.

A 100% IV means the market is pricing in a 68.3% probability (one standard deviation) that the stock price will either double or drop to zero. Practically, it means if I am taking a risk on in this situation, I want to be paid well for that risk - and so the premiums are super high when I sell such options - even far out of the money.

Anyway, here are the trades that helped me scalp a total of $295 in SPCX over 3 days I traded it.

See the first trade there (at the bottom of the screenshot) - I was in and out in less than 10 minutes for $70 in profit. And as I suspected, things slowed down after that and for the last trade, I had to wait for the next day to get to a point I could close it.

Trade Ideas

SPCX continues to have elevated implied volatility.

The stock IPO-d at $135. Right now, the 16∆ Put for August 21 is at $135, and is selling for a premium of $625. In my margin account, this trade needs a buying power of $4420. The theta is 13.258, so it decays by ~$13 per day. The probability of profit is 76%. Staying in the trade for just 16 days would return ~$200 if the price stays where it is or if it moves up. That would be about 5% return on the risked margin capital.

Thanks for reading. See you next week!

📌 Disclaimer: Nothing on this site is financial advice - I’m just here to entertain! Here’s my introduction, my trading philosophy, and some ground rules.