Day 110

Another winning week! My profits went up as the market continued to rally and VIX remained flat.

Market Recap

Over the last week, SPY moved up by nearly 2.3 percent and QQQ continued scorching up, moving up by nearly 5.5 percent.

SPY is at ~$737, and QQQ is on ~$710.

VIX continues to hover around 17.

Trading Update

I closed positions in the following:

- SPX

- Net: +$420

- UBER

- Net: +$33

- INTC

- Net: +$207

- HOOD

- Net: +$85

There were no new strategies deployed this week.

I made the trades in Intel I spoke about as an idea last week, making a nice little >$200 profit scalping winners as Intel continued to move up. I continue to have another similar position open hoping to squeeze some more gains before the bullish run in semiconductor hardware and memory stocks slows down.

I had multiple trades in SPX, a few Zero DTEs, some 5 to 7 DTEs, and 1 regular 45 DTE. I do have a learning as I got burnt on a Zero DTE when it breached into my Call Spread - luckily the damage was minimal since I had other SPX trades on, as well as the correction in tactics next day onwards that helped reverse the one loss.

So what is the learning?

I was always opening Iron Condors on every type of expiration - mostly classic, but sometimes skewed. By skewed, I mean uneven spreads on each side, for example, risk $10-wide on Put spread but $5-wide on Call spread.

In a highly bullish environment though, the skewed trade doesn’t quite work in a Zero DTE it seems - I was always worried that my Call Spread would get breached and be In the Money, and turned out I was right. So the learning now for me seems to be to have different tactics for different expirations. I have settled on the following setup:

- 45 DTE: Short Put Spread or Classic evenly spread Iron Condor, close at 50% profit or roll at 21-DTE.

- 5 - 7 DTE: Short Put Spread or Skewed Iron Condor, close for 25-50% profit, or roll at 3-4 DTE.

- Zero DTE: Short Put Spreads only, no management.

And how did I manage to thread around Pattern Day Trading with so many Zero DTEs? Well - I didn’t manage them at all! Just let them all ride into the sunset and expire - regardless of win or loss. I had Zero DTE trades on for 4 out of 5 days, losing 1 and winning 3.

How could I do that - when I don’t even backtest my strategies? Well - I trust that the math I am basing my trades on is accurate. Could it be wrong? Sure. But remember a key adage - all models are wrong, but some could be useful.

And what’s useful for me is the expected move calculation at the time I place my trades - I sell a Put Credit Spread at the expected move - and then trust both the expected move calculations as well as the probability around how many times those expected moves could be right or wrong. As long as the net amount gained from winners is more than what I lose, it’s all good. And I don't calculate anything, it's all visible on my TastyTrade options trading table.

And to top it off, I have over $2K in realized profits for the year. Which means every time I am placing a $10-wide or even a $20-wide condor, I am basically playing with house money, with nothing coming out of my pocket. Hopefully these little wins are the start of a snowball!

Here is the entire Year to Date P/L list for closed positions - I added previous week's list here for comparison.

I made $745 in realized premium profits this week, taking my realized gains for the year to date from $1,805 to $2,550.

Year to Date Realized Gains by Symbols Traded (Last week first, then current week)

Trade Ideas

Like I said earlier, I may continue with a similar setup in Intel.

I noticed MU also has great premiums but it is a very expensive stock.

An idea I explored was to sell a naked put to help finance a call at little to no cost.

Here is an example:

I sell a June 18 (~40 DTE) 120 Put and use the credit to finance a $135 Call for the same expiration. Per optionstrat (here), this setup results in a net credit of $65 - meaning I make money if the stock goes down slightly or shoots up, i.e, a neutral to bullish strategy. As shown below, my profit zone starts at around $119, and if it reaches $150, I could make over $1500.

But look at the downside risk, there is absolutely no room for error. So with that kind of downside risk, I get paid a little to take a shot at continued bullish momentum in Intel. Should I take it? I doubt I will. I need something simpler.

The general idea is to get some long delta exposure to the semiconductor market for the next 30 to 60 days. So whatever trades help me get there with a risk I am comfortable is what I will attempt.

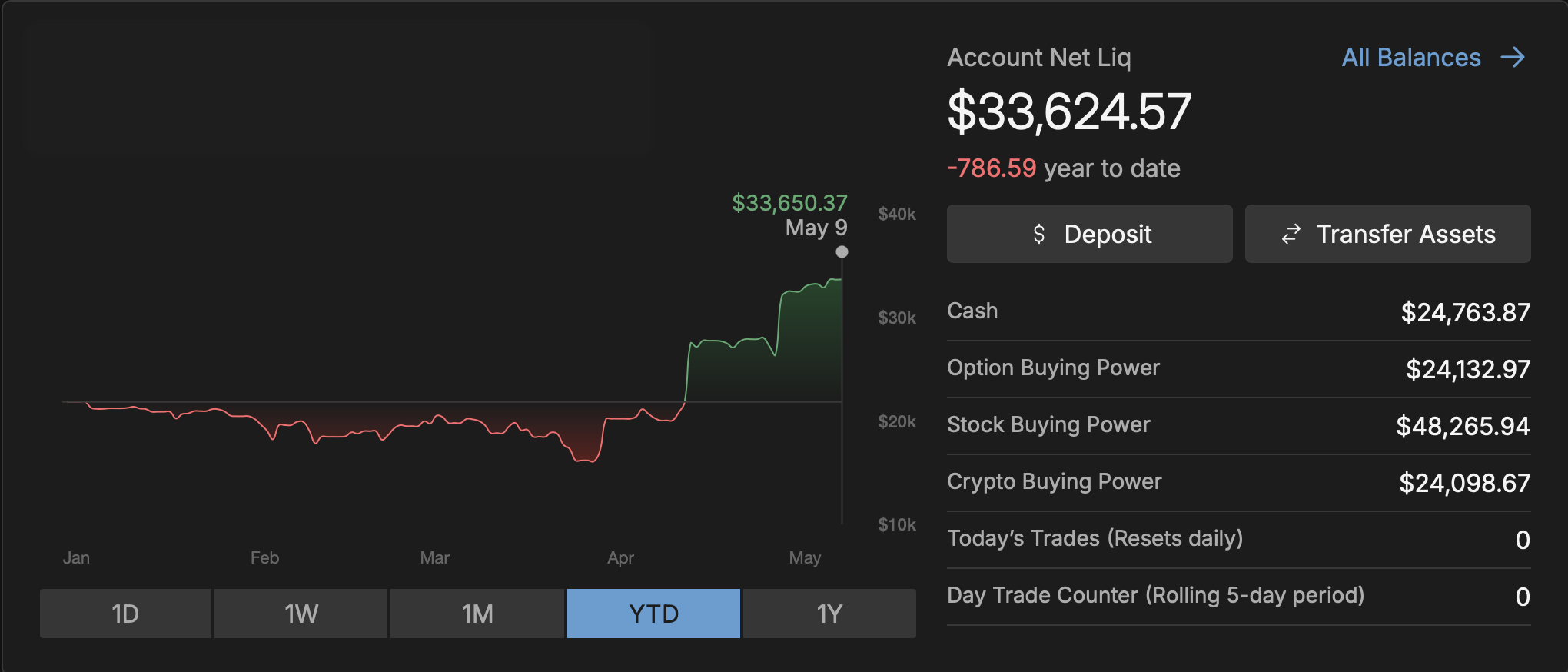

Portfolio Status

Here is the current portfolio status, including unrealized P/L.

I was looking through my last few write-ups and realized I have had only one losing week since March of this year (it was this one). That time covers a bearish market as well as a strong bullish run. I believe my conditioning is almost complete - I have enough tools to be profitable. Of course, my training isn’t since I believe learning to be a lifelong journey. Right now, I am heavily skewing strategies to be mostly handsfree, I can't really be monitoring my trades all day long because my primary source of income is my day job and not options trading. So the strategies and capital I deploy are customized to the constraints around my job - like trading before my work day starts or during my breaks.

Thanks for reading. See you next week!

📌 Disclaimer: Nothing on this site is financial advice - I’m just here to entertain! Here’s my introduction, my trading philosophy, and some ground rules.