The Arithmetic of Survival: "One Path" and the Geometry of Wealth

I am not a financial adviser and this is not financial advice. This is an introspective essay writing out the key ideas as understood from Mark Spitznagel's book I have read a couple of times now - "Safe Haven - Investing for Financial Storms".

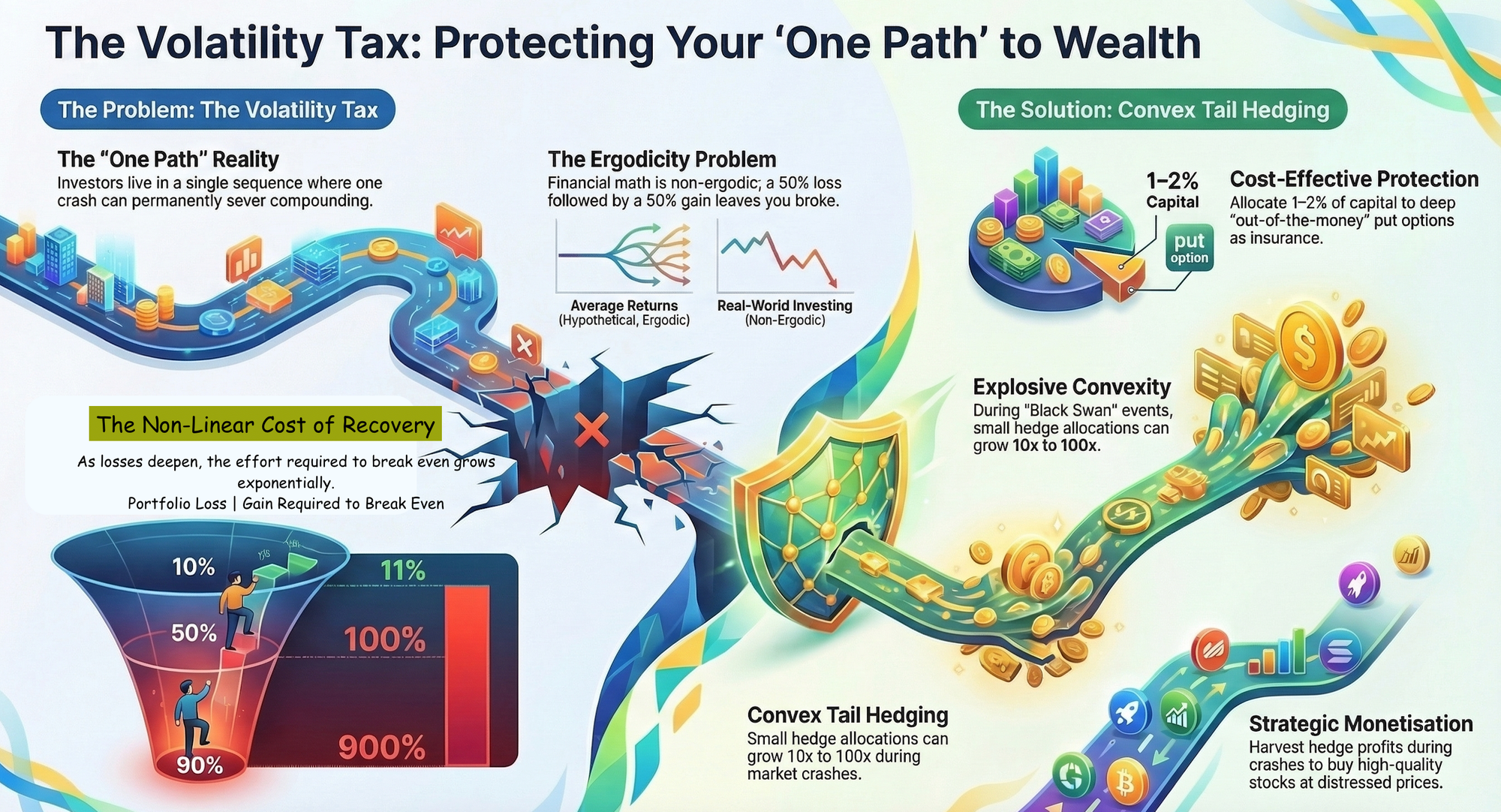

The conventional framework of modern finance rests upon the concept of "average" returns. Investors are taught to view risk through the lens of standard deviation and to expect that, over a long enough time horizon, their portfolio will gravitate toward an arithmetic mean. This perspective assumes a world of parallel possibilities where one might average the results of a thousand different lives. However, an investor does not live in an ensemble of possible outcomes; an investor lives in a single, non-repeating chronological sequence. This is the "One Path" reality. In this reality, the primary obstacle to wealth is not low returns, but the mathematical friction of loss, a concept Mark Spitznagel defines as the "Volatility Tax."

The Ergodicity Problem and the One Path

To understand Spitznagel’s philosophy, one must first distinguish between arithmetic and geometric averages. In a system where the average of a group is the same as the average of a single entity over time, the system is considered ergodic. Investing is fundamentally non-ergodic. If a gambler enters a casino with $1,000 and loses 50% on the first day, they require a 100% gain on the second day just to return to their starting capital. The arithmetic mean of these two days is 25% (the average of -50 and +100), yet the actual wealth remains unchanged.

In the "One Path" of a human life, the sequence of returns matters more than the average of those returns. A catastrophic "tail event" - a market crash of 30%, 40%, or 50% - does not merely lower the current balance of a portfolio. It severs the compounding chain. Because compounding works on the remaining principal, a deep drawdown removes the "seeds" required for future growth. The time spent recovering from a crash is "dead time," during which the investor is treading water while the relentless math of the Volatility Tax prevents forward progress.

Adopting the philosophy of Amor Fati - the love of one’s fate - becomes a practical necessity in this context. An investor must accept the reality of the single path they are on, including the certainty that extreme negative events will occur. Rather than wishing away volatility or pretending it can be smoothed out through diversification alone, the practitioner of Amor Fati accepts the crash as an inherent feature of the system and prepares the portfolio to turn that fate into an advantage.

The Mechanics of the Volatility Tax

The Volatility Tax is the hidden cost of drawdowns. It is a non-linear penalty. As losses grow, the effort required to recover grows exponentially. A 10% loss requires an 11% recovery, a manageable hurdle. However, a 50% loss requires a 100% gain, and a 90% loss requires a 900% gain. Most investors focus on "Alpha," or the ability to pick winning stocks that outperform the index. Spitznagel argues that the most effective way to increase terminal wealth is to focus on "Cost-Effective Risk Mitigation" - minimizing the Volatility Tax so that compounding can operate unimpeded.

Traditional safe havens, such as gold or government bonds, often fail this test. While they may provide some protection during a crash, they frequently carry a high opportunity cost during bull markets. If an asset protects you during a crash but drags down your returns by 4% every year for a decade, you may end up with less wealth than if you had simply endured the crash. A true safe haven must be cost-effective; it must provide a disproportionate payout during a crisis while requiring a minimal capital allocation during normal times.

The Architecture of the Tail Hedge

The solution Spitznagel proposes is the implementation of a tail-risk hedge using explosive, convex instruments. For a standard equity portfolio, this typically involves buying deep out-of-the-money (OTM) put options.

The structure of this hedge is specific:

- Low Capital Allocation: The investor allocates a small, fixed percentage of the portfolio - perhaps 1% to 2% annually - to purchase these options. This is viewed as a recurring operating expense, similar to fire insurance on a physical asset.

- Deep OTM Strikes: The options are selected at strikes significantly below the current market price, often 30% lower. In a normal market, these options will expire worthless.

- Explosive Convexity: Because these options are so far "out of the money," they are inexpensive. However, during a systemic crash, two things happen simultaneously: the market price approaches the strike, and Implied Volatility (IV) spikes. This dual action causes the value of the puts to increase not linearly, but exponentially. A hedge that cost 1.5% of the portfolio can potentially grow by 10x, 50x, or 100x in value during a true "Black Swan" event.

This is the "Safe Haven" in action. It is not designed to track the market or provide steady income. It is a power-law asset that sits dormant until the exact moment the "One Path" encounters a cliff.

Monetization: Turning Defense into Offense

The ultimate goal of the tail hedge is not the profit from the hedge itself, but the liquidity it provides. In a market crash, liquidity vanishes. Assets are sold at distressed prices because investors are forced to meet margin calls or are driven by psychological panic. The hedged investor, however, finds themselves in the opposite position.

When the market drops 30% and the VIX (the "Fear Index") spikes to 40 or 50, the tail hedge provides a massive infusion of cash. The practitioner of this strategy must then "monetize" or harvest the hedge. This involves selling the hyper-inflated options and using the proceeds to buy more of the underlying equity index or high-quality stocks at their lows.

This creates a "crossover" effect in terminal wealth. While the unhedged investor is waiting years for their portfolio to return to its previous peak, the hedged investor has used their payout to increase their share count at the bottom. When the recovery eventually begins, the hedged investor is compounding on a larger base of shares. Over twenty or thirty years, this cycle of protecting the downside and aggressively buying the lows results in significantly higher final wealth than a passive buy-and-hold strategy.

The Behavioral Discipline of the Strategy

The difficulty of Spitznagel’s approach is not the mathematics, but the psychology. To maintain a tail hedge, one must be willing to "lose" money on the insurance premiums for years at a time. In a prolonged bull market, the hedge will look like a mistake. Critics will point to the 1.5% annual drag and suggest that the capital could be better spent elsewhere.

This is where the internalizing of Amor Fati is tested. The investor must love the process of protection as much as the process of growth. They must accept that the "loss" on the hedge is actually a "payment" for the certainty of survival. By clipping the left tail of the distribution - removing the possibility of total ruin - the investor gains the psychological fortitude to stay invested during periods of extreme fear.

Implementation for the Modern Portfolio

For an investor managing a standard portfolio, such as $100,000 in an S&P 500 ETF (SPY), the practical steps are mechanical. One might spend $125 every month to buy puts that are 30% below the market, expiring in 60 days, and rolling them every 30 days.

The strategy remains dormant until volatility regimes shift.

- In Low Volatility (VIX 10-15): The hedge is a quiet expense.

- In Rising Volatility (VIX 20-30): The hedge begins to stabilize the portfolio's fluctuations.

- In Extreme Volatility (VIX 40+): The hedge is harvested for cash.

This matrix ensures that the investor is always a buyer of volatility when it is cheap and a seller of volatility when it is expensive.

Conclusion

Mark Spitznagel’s unique insight is that the greatest threat to an investor is not a lack of opportunity, but the mathematical reality of the single path. By rejecting the comfort of arithmetic averages and embracing the harsh geometry of the Volatility Tax, an investor can structure a portfolio that does more than survive a crash.

How the Math Changes Your Life

The "explosive" part of the payout refers to Convexity. If the market drops 30%, a 1.5% hedge typically returns 10x to 50x its cost.

- The Survival Gap: After a 50% crash (like 2008), it took the S&P 500 5.5 years just to get back to zero. For those 5.5 years, the unhedged investor made $0 in new wealth.

- The Power of Reinvestment: If your hedge pays out $15,000 during that same 50% crash, you use that money to buy SPY at half price. When the market eventually recovers, that $15,000 "seed" has doubled to $30,000.

The Insight: While the payout doesn't "fix" the loss; it still shortens the time it takes for your net worth to reach its next all-time high.

In Spitznagel's "One Path," the person who recovers in 2 years instead of 6 years ends up significantly wealthier 20 years later because they spent more time compounding and less time "treading water."

Through the disciplined use of convex tail hedges, the crash becomes the very mechanism that accelerates long-term compounding. This is the synthesis of risk management and wealth creation. It is the realization that by preparing for the worst possible fate, one secures the best possible outcome on the only path that matters. Amor Fati is not merely a stoic resignation to the market's whims; it is the strategic foundation for a life of compounding.

References

- Safe Haven - Investing for Financial Storms - By Mark Spitznagel: https://www.amazon.com/dp/1119401798/?bestFormat=true&k=safe%20haven%20mark&ref_=nb_sb_ss_w_scx-ent-bk-ww_k1_1_15_de&crid=15FI3ZQNRDUXI&sprefix=Safe%20Haven%20mark